-

Renewable Energy/

Energy/

Sustainability

Explaining ASEAN’s Renewable Energy Bottleneck

Why abundant renewable capacity no longer guarantees usable power—and what that means for Southeast Asia’s energy transition.

- Candice Lim

ASEAN’s renewable energy transition is no longer constrained by ambition or resource availability—but by the systems designed to carry, store, and govern power. Across Southeast Asia, solar, wind, hydro, and geothermal capacity has expanded rapidly over the past decade. National targets have been revised upward, deployment has accelerated, and regional commitments now point toward a significantly higher renewable electricity share by 2030.

Yet a persistent gap remains between installed renewable capacity and usable, reliable power. Curtailment, grid congestion, storage shortfalls, and rigid market structures increasingly determine outcomes. The challenge facing ASEAN today is not whether clean energy can be generated—but whether existing systems can absorb, transmit, and deploy it effectively.

Author’s Note

A few years ago, I noticed solar panels being installed on the rooftops of HDB flats in the mature estate where my parents live. It was a small, everyday signal—but one that reflected a broader regional shift. That observation led me to examine how solar energy and other renewables were scaling across Southeast Asia, and eventually to produce Renewing ASEAN: Energy Goals & Achievements, the first snapshot report by The Future Atlas, published in May 2025.

More recently, similar installations have appeared on the rooftops of the HDB estate where I now live. Around the same time, regional announcements—from floating solar proposals in Malaysia to offshore and hybrid renewable projects elsewhere in ASEAN—raised a more fundamental question: if renewable capacity across Southeast Asia has been expanding steadily, why has it not yet translated into renewable energy becoming a primary, reliable power source for the region?

Capacity Gains Are Real—But Not Sufficient

In May 2025, The Future Atlas published Renewing ASEAN: Energy Goals & Achievements, capturing the region at a moment when renewable ambition, installed capacity, and national commitments across Southeast Asia were accelerating in parallel. That snapshot focused on targets and capacity. What the evidence now suggests is that the limiting factor is no longer ambition but system design.

Renewable energy has made significant strides across ASEAN. Recent regional planning documents show that installed renewable power capacity—especially solar and wind—is on track to exceed earlier targets.

In October 2025, ASEAN energy ministers endorsed the APAEC 2026-2030, setting a bold target of 45% renewable energy in total installed capacity by 2030. This represents a significant scaling of ambition from the previous 35% goal. This shift reflects a move from simply ‘adding capacity’ to ‘integrating generation’, as energy intensity targets have also been tightened to a 40% reduction by 2030.

These measures reflect political will and growing deployment success. But the story does not end with capacity.

A New Constraint: Capability, Not Capacity

What has become increasingly clear is that renewable capacity growth no longer equates to reliable, accessible energy. The limits have shifted from physical generation to the ability to move energy where it is needed and use it reliably.

Three structural realities now dominate outcomes:

- Grid Infrastructure Lagging Behind

While many countries have deployed significant renewable capacity, the electricity grids themselves are not yet ready to absorb and transfer low-carbon power efficiently.

A regional Asian Development Bank report notes that Asia and the Pacific’s grid infrastructure, including in Southeast Asia, is not prepared for the accelerated pace of the clean energy transition. Insufficient interconnectivity and limited grid capacity lead to technical losses and inefficiencies that constrain renewable deployment. (SEADS)

- Massive Investment Gaps in Interconnectivity

Developing an interconnected ASEAN Power Grid (APG)—the core vision for regional power cooperation—requires enormous financial resources. Analysts estimate at least US$100 billion in investment to build the necessary transmission lines across ASEAN. (Eco-Business)

In October 2025, the ADB and World Bank launched a joint financing initiative to mobilise funding for the APG, with ADB pledging up to $10 billion and the World Bank contributing seed funding and technical support. (ASEAN Centre for Energy (ACE))

Despite these initiatives, the pace of grid interconnection remains slower than renewable deployment. An APG vision first articulated in 1999 (and revitalized in 2016) remains targeted for full operation by 2045, highlighting long project cycles and coordination challenges. (World Bank)

- Storage and Flexibility Are Still Emerging

Beyond transmission, energy storage and system flexibility—essential for handling intermittent sources like solar and wind—remain underdeveloped at scale across ASEAN. A detailed regional energy assessment notes that battery storage and pumped hydro deployment are limited, while demand-side response programs are still in early stages in most countries. Without this flexibility, grids cannot reliably integrate high shares of renewables. (EU-ASEAN Business Council)

What the data now reveals is not a shortage of renewable capacity, but a growing mismatch between where energy is generated and how existing systems are designed to move, store, and price it.

[For a country-by-country overview of ASEAN’s renewable targets and capacity trajectories, see our earlier snapshot Renewing ASEAN: Energy Goals & Achievements (May 2025).]

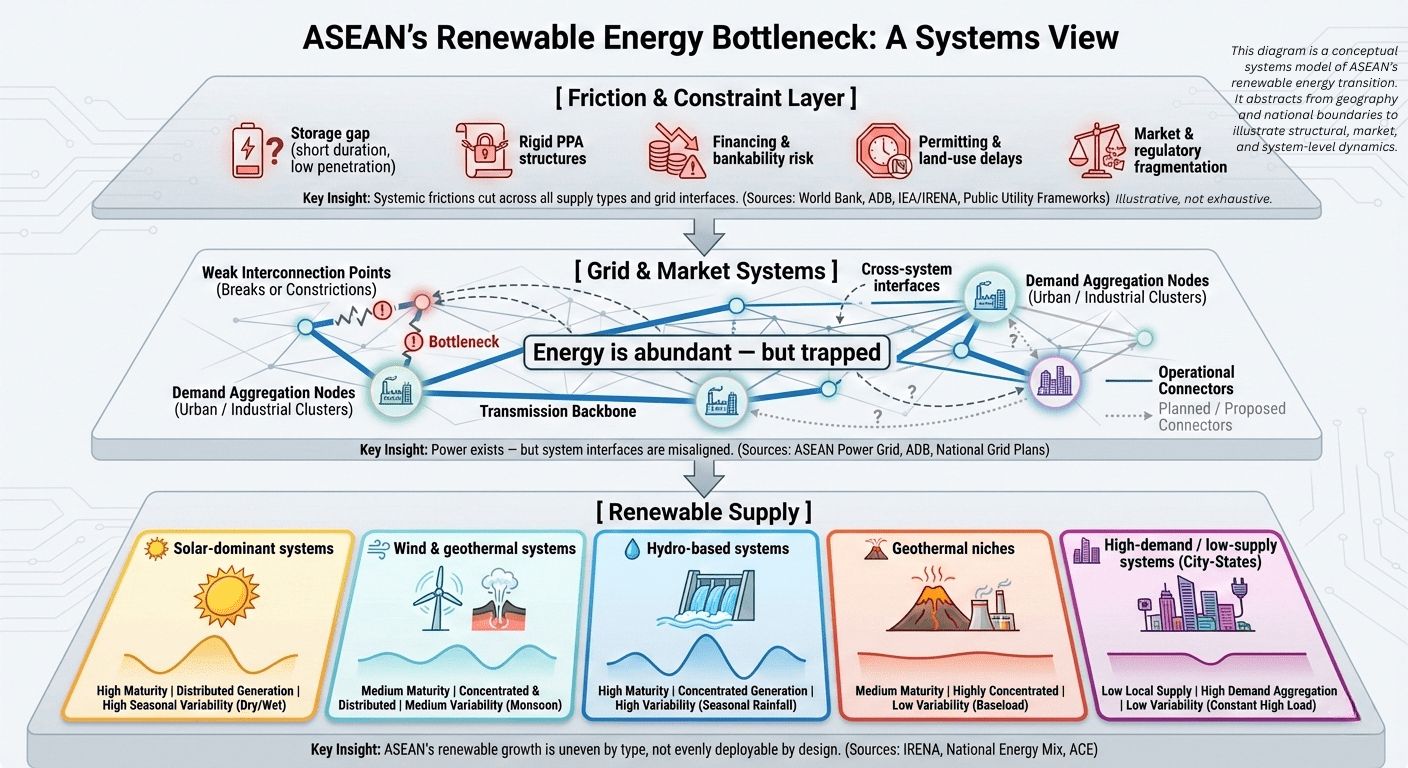

The Systems-level Diagram: How Supply, Systems, and Friction Interact

To make sense of this disconnect, it became necessary to step away from geography and instead view ASEAN’s renewable energy transition as a system. The diagram above presents a conceptual, systems-level view of the region’s energy landscape—one that separates renewable supply potential from the grid, market, and regulatory structures that shape how power actually moves.

Rather than mapping countries, it highlights three interacting layers: renewable supply profiles, grid and market systems, and the frictions that cut across them. What emerges is a clearer diagnosis of the bottleneck facing the region today: energy is increasingly abundant, but the systems designed to carry, price, and integrate it have not kept pace.

Together, these layers explain why renewable energy progress sometimes looks superficially strong but fails to translate into usable, reliable power at scale.

Why This Matters for ASEAN’s Energy Futures

The result of these constraints is a situation where:

- Renewable projects can be built yet struggle to deliver energy reliably because the grid cannot support high volatility and long-distance transfer.

- Investment risk remains elevated because developers price in grid uncertainty and policy ambiguity.

- Regional cooperation—while politically endorsed—still faces technical, regulatory, and financial hurdles.

This shift from capacity to capability helps explain why even nations with ambitious renewable targets still rely on fossil backup or limited energy imports.

What Actually Moves the Needle Next

To convert capacity into capability, three priorities should take centre stage:

- Grid Modernisation and Regional Integration

Cross-border interconnections and harmonised grid codes are essential. The ASEAN Power Grid vision aims precisely at this, but it requires deep infrastructure investment, coordinated regulation, and political alignment. (World Bank)

The most significant proof-of-concept for this integration is the Lao PDR-Thailand-Malaysia-Singapore Power Integration Project (LTMS-PIP). Launched in its multilateral phase in June 2022, it marked the first time power was traded across three borders among four ASEAN member states. By successfully navigating the technical and regulatory complexities of multi-country transmission, the LTMS-PIP serves as the working blueprint for the broader ASEAN Power Grid. It demonstrates that while the ‘bottleneck’ is real, the architecture for multilateral trade is no longer just theoretical—it is an operational reality that now requires scaling.

- Storage at Scale

Energy storage must transition from project-by-project to system-wide planning. Without it, high penetration of intermittent renewables will remain difficult to manage reliably.

- Market Reform and Policy Certainty

Expanding the regional trade of Renewable Energy Certificates (RECs) will be vital to monetize green electrons that are currently ‘trapped’ by local grid congestion.

Conclusion: From Ambition to Architecture

ASEAN’s renewable energy transition narrative has matured. What once was primarily a story of capacity additions is now a systems problem. Generators and targets are only one part of the equation—the real test is whether clean energy can be integrated, transmitted, and used reliably.

This article highlights that system bottlenecks are not just technical—they are economic, regulatory, and geopolitical. Addressing them is the next frontier for Southeast Asia’s energy transformation.

Key Sources and Further Reading

- 8th ASEAN Energy Outlook — ASEAN Centre for Energy (2024). Regional energy trends and renewable capacity projections. (ASEAN Centre for Energy (ACE))

- ASEAN Renewable Energy Long-Term Roadmap — ACE (2025). Strategic framework for decarbonisation and grid flexibility needs. (ASEAN Centre for Energy (ACE))

- ADB / World Bank APG Financing Initiative — Press release and financing details for ASEAN Power Grid deployment. (ASEAN Centre for Energy (ACE))

- ADB Grid Readiness Report — Analysis of grid constraints across Asia Pacific, including Southeast Asia. (SEADS)

- Transmission Investment Needs — ADB estimate of investment required for ASEAN grid interconnectivity. (Eco-Business)

- Enerdata (2024). ASEAN aims for 45% of power capacity from renewables by 2030.

- The Investor Vietnam (2024). ASEAN sets ambitious energy targets.

- Continue Reading