- A USRF™ Scenario Perspective: March 2026

Energy Security Signals Across ASEAN

By early March 2026, tanker flows through the Strait of Hormuz had effectively collapsed, prompting an unprecedented 400‑million‑barrel release from emergency oil reserves and turning Southeast Asia’s energy security from a policy discussion into an active stress test. Using The Future Atlas Urban Systems Risk Framework (USRF™), this article examines how the chokepoint disruption is transmitting shocks through the region’s interconnected energy, fiscal and infrastructure systems.

- Candice Lim

Recent geopolitical developments in the Middle East have reintroduced significant uncertainty into global energy markets. While Southeast Asia is geographically distant from the conflict, its energy systems remain closely tied to global oil and liquefied natural gas (LNG) supply chains.

A large share of Asia’s imported fuel, and a particularly high share of imports into hubs such as Singapore, originates from or passes through the Gulf. As a result, geopolitical instability can quickly translate into price volatility, shipping risk and investment uncertainty across ASEAN energy markets.

From a USRF™ perspective, the central question is not only whether physical supply is disrupted. The more important issue is how different trajectories of the crisis transmit pressures through the region’s energy, fiscal and infrastructure systems.

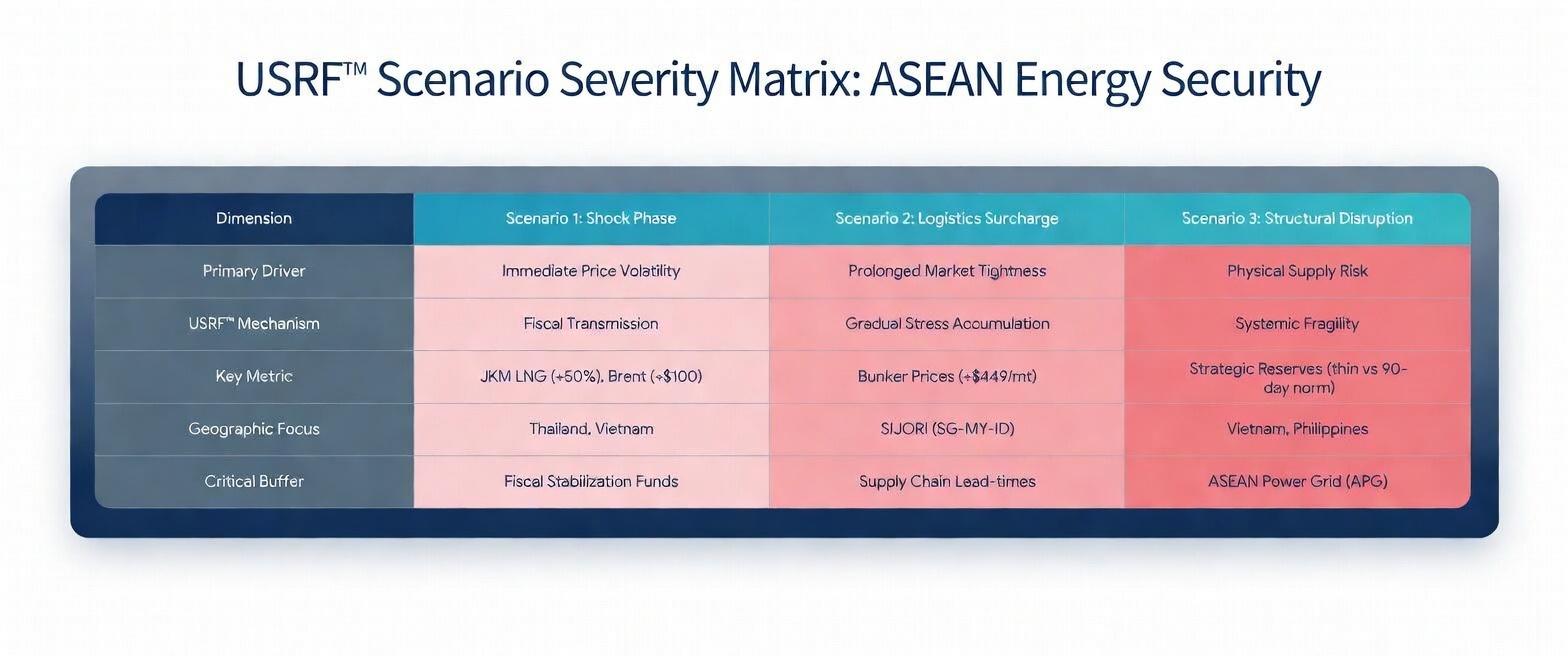

Three scenarios illustrate where those pressures may emerge.

Scenario 1: The Shock Phase (Initial Volatility)

The intensification of conflict in late February 2026 triggered an immediate Shock Phase. Within days, the JKM (Japan–Korea Marker) LNG benchmark spiked by well over 50%, while Brent crude surged back above 100 USD per barrel as tanker traffic through Hormuz collapsed.

From a USRF™ lens, this phase is characterised by fiscal transmission. In markets like Thailand and Vietnam, governments have already begun tapping stabilisation funds and using temporary price caps to shield consumers from the initial shock.

- In Thailand, the Oil Fuel Fund has been deployed to hold down diesel prices while officials scramble to secure alternative supplies.

- In Vietnam, the fuel price stabilisation fund and temporary tariff reductions are being used to slow the pass‑through of global price spikes into retail markets.

These measures soften the immediate social impact, but they are not cost‑free. The primary medium‑term risk is the energy–inflation lag: if elevated fuel and wholesale power costs persist, fiscal strain on utilities and public budgets can quietly squeeze out capital for grid modernisation and renewable‑energy support.

In other words, the system may avoid a visible price shock today, only to experience delayed under‑investment in critical infrastructure tomorrow.

Scenario 2: Prolonged Market Tightness (The Logistics Surcharge)

As the disruption extends into its third week, the crisis has evolved into Prolonged Market Tightness. With tanker transits through Hormuz down by roughly 90% at times, the cost of securing alternative routes and suppliers has risen sharply.

In Singapore, the world’s largest bunkering hub, LNG bunker prices rose by about 449 USD per metric ton in the first week of March alone. At the same time, war‑risk premiums for maritime insurance on Gulf‑exposed routes have jumped to multi‑year highs, and charter rates for large tankers have spiked.

Through a USRF™ perspective, this is a phase of gradual stress accumulation rather than sudden failure. Higher bunker and freight costs do not only appear at the pump; they diffuse through industrial production and construction value chains.

- Steel, cement and other high‑energy‑intensity materials face rising input costs.

- Shipping‑dependent sectors see margins compressed as logistics and insurance costs climb.

- Project budgets that were already tight struggle to absorb unexpected cost escalations.

In the Singapore–Johor–Riau (SIJORI) Growth Triangle, where manufacturing, logistics and data‑centre development are tightly coupled to global shipping routes, this evolving “logistics surcharge” erodes project margins and raises delivery risk.

If elevated costs persist, they could stall or re‑sequence major infrastructure projects across SIJORI—not because plans are cancelled on paper, but because financing structures and construction schedules cannot easily accommodate sustained cost inflation.

Scenario 3: The Active Blockade (Structural Supply Disruption)

With flows through Hormuz still severely constrained and key export terminals idled, Southeast Asia is now confronting the risk of Structural Supply Disruption.

Force majeure declarations by major suppliers such as Qatar have temporarily sidelined a large share of its roughly 20% contribution to global LNG exports, forcing ASEAN buyers to compete on an already tight spot market for replacement cargoes. Even when alternative volumes exist in the Atlantic Basin, redirecting them is slow and expensive.

Under USRF™, this scenario exposes systemic fragility in nations with limited strategic buffers.

- Vietnam’s current regulations require around 20 days of commercial petroleum reserves, and national strategic reserves remain modest compared with IEA‑style 90‑day benchmarks.

- The Philippines has shifted selected government offices to a four‑day work week and expanded work‑from‑home arrangements, explicitly to conserve transport fuel and electricity.

These measures underline a critical point: physical supply has so far been maintained, but policy space is narrow. In USRF™ terms, both countries sit close to a critical vulnerability threshold—where demand‑side measures and fiscal tools can buy time, but protracted disruption would begin to test reserve systems, budgets and social tolerance for conservation.

This episode also reframes cross‑border electricity interconnections—particularly the ASEAN Power Grid (APG). In this context, the APG is not only a decarbonisation instrument; it is a key regional buffer that can help prevent localised fuel price shocks and supply disruptions from escalating into wider economic stress.

USRF™ System Pressure Signals: The Hormuz shock is exposing four core transmission points across ASEAN energy systems:

- Fuel import dependence

Heavy reliance on Gulf oil/LNG routed through Hormuz creates immediate price/supply volatility. - Electricity demand growth

Rapid urban and industrial expansion—along with the rise of digital infrastructure and data centres—amplifies the system‑wide impact of wholesale energy cost spikes. - Power system diversification

Limited renewable integration and flexibility in many ASEAN power systems leave utilities highly exposed to fossil‑fuel price transmission and supply risks. - Regional grid interconnection potential

The ASEAN Power Grid (APG) emerges as a critical buffer, enabling cross‑border power trade that can prevent localised shocks from triggering wider system stress.

Strategic Transition Pressure

The current crisis also surfaces a longer‑term strategic question.

Southeast Asia must expand energy capacity to support economic growth while accelerating its transition toward lower‑carbon and more resilient systems. This dual challenge is becoming increasingly complex.

Electricity demand is rising rapidly as urbanisation, industrialisation and digital infrastructure expand. Meeting this demand will require large‑scale investment in new generation capacity, grid reinforcement and flexibility resources such as storage and demand response.

At the same time, climate commitments and global capital markets are pushing the region toward cleaner energy sources and stronger resilience standards. Events such as the present Middle East crisis show how import dependence and energy‑transition timelines intersect, shaping both infrastructure investment and policy priorities.

If fossil‑fuel markets remain volatile, the economic case for renewables, efficiency and regional power interconnections becomes stronger. Yet financing constraints, governance challenges and regulatory barriers can still slow deployment.

In this context, the energy transition is no longer only a climate objective. It is increasingly a core energy‑security strategy: reducing exposure to external shocks by diversifying supply, upgrading grids and managing demand more intelligently.

A Systems Signal for the Region

From a USRF™ perspective, the key question is not just whether the current crisis disrupts Southeast Asia’s energy supply today, but whether these shocks accelerate the structural reconfiguration of the region’s energy architecture.

Central to this evolution is the ASEAN Power Grid (APG). Within the USRF™ framework, the APG acts as the region’s primary binding system.

By enabling multilateral trade in “renewable electrons”—linking Lao PDR’s hydropower, Vietnam’s prospective offshore wind and Indonesia’s solar potential—the APG can reduce Transmission Risk: the process by which a single geopolitical disruption in the Gulf cascades into system‑wide stress across Southeast Asian urban centres.

Without the APG acting as a physical and market buffer, ASEAN economies remain comparatively unbound, forcing each nation to absorb volatility individually through subsidies, emergency procurement and ad‑hoc conservation. In such a configuration, every future chokepoint crisis risks retriggering the same cycle of fiscal strain and reactive policy.

By contrast, a more fully realised APG—backed by clear market rules, adequate cross‑border capacity and integrated planning—would allow countries to:

- Share surplus low‑carbon generation across borders

- Smooth local fuel‑supply disruptions

- Reduce the marginal impact of global fuel price spikes on domestic consumers and industry

In that world, an external shock still hurts, but it is less likely to metastasise into a regional economic event.

The current crisis is therefore more than a geopolitical episode. It is a systems signal that ASEAN’s fuel‑centric energy architecture is increasingly misaligned with the scale and nature of external risks.

In this sense, the ASEAN Power Grid is no longer just a long‑term decarbonisation goal. It is becoming an increasingly central piece of regional energy security and economic resilience over the coming decade—one of the few levers that can simultaneously cut emissions, deepen markets and blunt the impact of shocks that begin far from Southeast Asia’s shores.

- Continue Reading