-

The Future Atlas Watchlist

Energy & Decarbonisation

Southeast Asia Energy & Decarbonisation Watchlist

Projects, power procurement and resource infrastructure I’m watching

Energy risk has moved back into the foreground. Across Southeast Asia, the pressure is starting to show up in projects: solar farms entering construction, industrial power procurement changing, cross-border clean-power plans taking shape, and resource infrastructure being asked to do more with land, water and waste.

- Candice Lim

Energy is no longer sitting quietly in the background of the built environment. The Middle East war has pushed fuel exposure back into business planning, freight costs, electricity tariffs and government support packages. Reuters reported that the World Bank expects energy prices to rise 24% in 2026 because of disruptions linked to the war, while ASEAN economic ministers have warned that the conflict could slow regional growth through energy, freight, insurance and logistics pressures. (Reuters)

For Southeast Asia, this is not a distant macro story.

The region still depends heavily on imported fuel, even as countries move toward 2030 climate and energy targets. In Singapore, the overall electricity tariff for 1 April to 30 June 2026 increased by an average of 2.0% before GST from the previous quarter, while the carbon tax rose to S$45/tCO₂e from 1 January 2026 for 2026 and 2027. (SP Group)

That is the pressure behind this watchlist.

The projects below are not all at the same stage. Some are already under construction. Some are in delivery. Some are still in development or long-range planning. One row captures a buildout pattern rather than a single project.

I have kept those caveats visible because they matter. A project in construction says one thing about the market. A planned corridor says another. Both can be useful to watch, as long as they are not treated as the same kind of evidence.

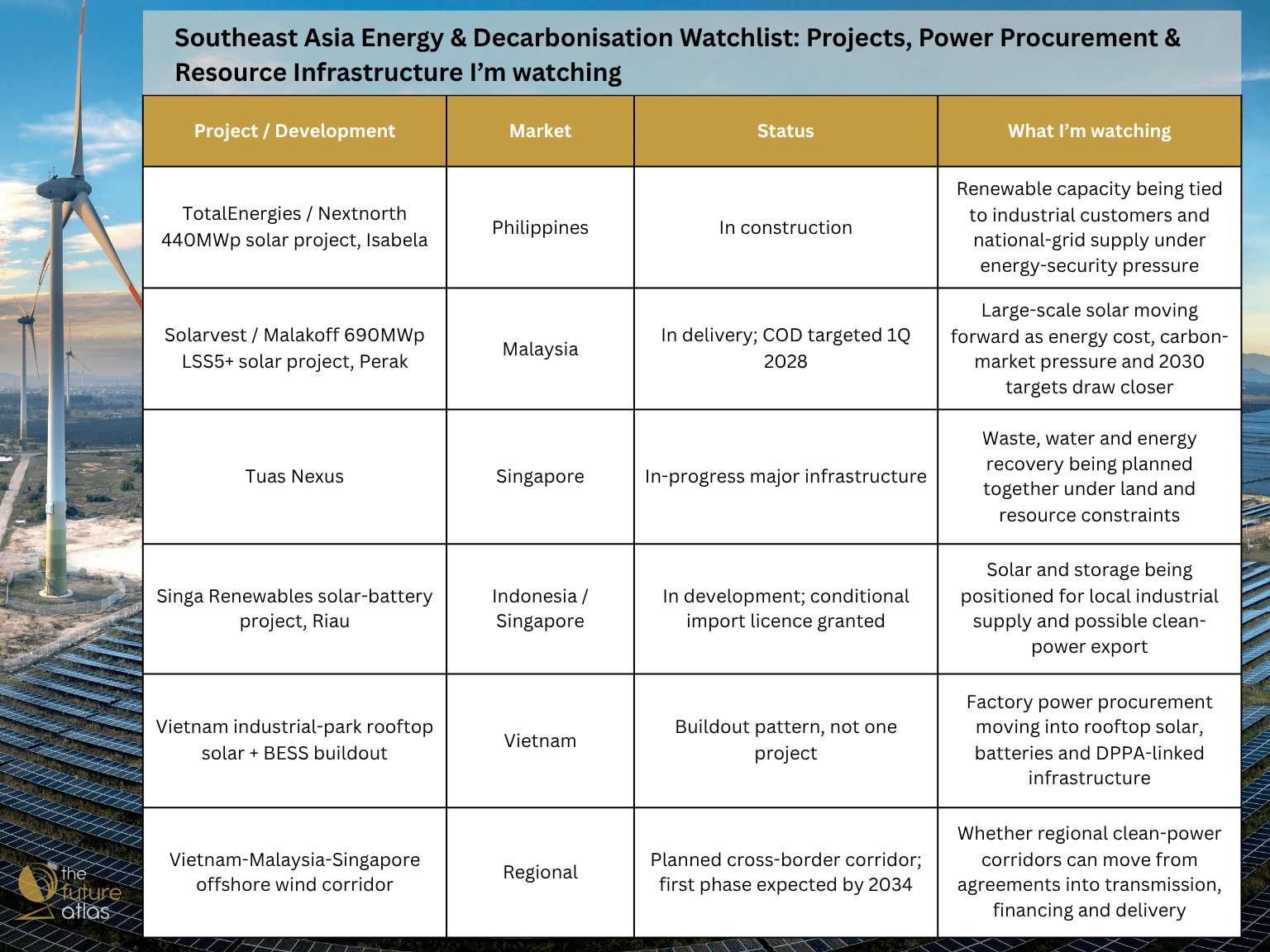

The Isabela solar project in the Philippines is the most current marker in this list. TotalEnergies and Nextnorth reached financial close and began construction of the 440MWp solar project in April 2026. Reuters reported that the US$300 million project is expected to come online by end-2027, with half of the electricity to be sold to industrial clients and the rest supplied to the national grid under the Philippines’ fourth renewable energy tender. (TotalEnergies.com)

That mix matters. Industrial clients need cost visibility and power reliability. The grid needs domestic renewable capacity. Energy security, decarbonisation and corporate power procurement are beginning to sit in the same project.

Malaysia’s Perak LSS5+ project is another large marker. Solarvest says the 690MWp solar project in Larut and Matang, Perak, spans nearly 1,400 acres, is scheduled for commercial operation in 1Q 2028, and is expected to generate up to 970,000MWh of clean energy annually. (Solarvest)

The project sits inside a broader Malaysian moment. Carbon-tax details are still settling, the national carbon-market framework is taking shape, and industrial users are watching energy cost more closely. A solar farm of this scale becomes more than a generation asset. It becomes part of the country’s industrial competitiveness story.

Tuas Nexus is older in timeline, but still important. It is included here because it shows another version of decarbonisation: resource infrastructure designed around co-location. NEA says the Integrated Waste Management Facility and PUB’s Tuas Water Reclamation Plant will be co-located at Tuas View Basin to maximise energy and resource recovery from solid waste and used-water treatment. PUB similarly describes Tuas Nexus as integrating used-water and solid-waste treatment to maximise energy efficiency, generation and resource recovery while maintaining a small footprint. (National Environment Agency)

This is less spectacular than a new solar farm, but probably just as important. Dense cities cannot treat waste, water, energy and land as separate problems forever.

The Singa Renewables solar-battery project in Riau is a different kind of watch item. TotalEnergies and RGE announced the solar and battery project in May 2025, with Singapore’s Energy Market Authority granting a conditional licence for up to 1GW of clean firm power imports to Singapore. TotalEnergies says the project will also supply electricity to local industry in Indonesia. (TotalEnergies.com)

This is still in development, so it should not be read like a project already under construction. Its relevance is the corridor logic: solar, storage, industrial supply, export approval, and Singapore’s long-term search for low-carbon electricity imports.

Vietnam’s industrial-park rooftop solar and BESS buildout is not one project. It is a pattern. VnEconomy reported in April 2026, citing Ministry of Industry and Trade data, that rooftop solar capacity at Vietnam’s industrial parks exceeded 3,200MWp during 2024–2025, with about 25% of systems integrated with battery energy storage systems. (VnEconomy)

That figure is useful because it shows distributed energy moving into industrial land. It also fits with Vietnam’s direct power purchase framework and the pressure on manufacturers to secure cleaner, more predictable electricity. The built environment angle is not only the factory roof. It is the park, the grid interface, the battery system, and the procurement model behind it.

The Vietnam-Malaysia-Singapore offshore wind corridor is the most long-range item here. Reuters reported in October 2025 that Malaysia’s energy minister said the first phase of the 2,000MW project is expected by 2034, with 700MW for Malaysia’s domestic use and 1,300MW for export to Singapore. (Reuters)

That timing is far out, so the row has to be read carefully. It is not near-term delivery. It is a test of whether Southeast Asia can build the kind of cross-border clean-power corridor that decarbonisation targets increasingly assume will exist.

Taken one by one, these projects sit in different boxes: solar, waste, water, storage, industrial parks, offshore wind.

Read together, they say something sharper.

Energy cost is becoming a project issue.

Carbon cost is becoming a project issue.

Industrial power procurement is becoming a project issue.

Grid access, land, batteries, water and waste are becoming part of the same conversation.

The next phase of decarbonisation in Southeast Asia will not only be measured by targets. It will show up in which projects can secure power, manage cost, prove carbon value, and still get built.

Sources

- Reuters, “World Bank forecasts 24% surge in energy prices in 2026 due to Middle East war,” April 2026. (Reuters)

- Reuters, “ASEAN economic ministers say Middle East war could significantly slow regional growth,” May 2026. (Reuters)

- SP Group, “Electricity Tariff Revision for the Period 1 April to 30 June 2026.” (SP Group)

- National Climate Change Secretariat Singapore, “Carbon Tax.” (National Climate Change Secretariat)

- TotalEnergies, “Philippines: TotalEnergies and Nextnorth Reach Financial Close and Start Construction of a 440 MW Solar Project,” April 2026. (TotalEnergies.com)

- Reuters, “TotalEnergies and Nextnorth begin building $300 million Philippine solar farm,” April 2026. (Reuters)

- Solarvest, “Solarvest Powers Malaysia’s Energy Security With Nation’s Largest LSS5+ Solar Project,” April 2026. (Solarvest)

- NEA, “Integrated Waste Management Facility.” (National Environment Agency)

- PUB, “Tuas Water Reclamation Plant / Tuas Nexus.” (PUB, Singapore’s National Water Agency)

- TotalEnergies, “Indonesia-Singapore: TotalEnergies and RGE Reach New Milestone in Large-Scale Solar and Battery Storage Project,” May 2025. (TotalEnergies.com)

- Energy Market Authority Singapore, “Singapore Grants Conditional Licence to Singa Renewables for Electricity Imports from Indonesia,” May 2025. (Energy Market Authority)

- VnEconomy, “Vietnam’s energy sector seeks qualitative growth,” April 2026. (VnEconomy)

- Reuters, “Vietnam-Malaysia-Singapore offshore wind project to complete first phase by 2034, Malaysia energy minister says,” October 2025. (Reuters)

- Continue Reading